The institutional rise of growth lending in european tech: a comparison to the US

March 2026

March 2026

Over the past decade, growth lending has evolved from a niche tool to a core part of how technology companies finance their growth. In the US, it’s well established – used across different stages of a company’s life and supported by a deep institutional market.

Whilst it’s by no means a new financing solution in Europe, growth lending is maturing on a different timeline. Changes across capital markets, regulation, and venture capital are reshaping how companies and investors think about financing, and accelerating Europe’s shift toward a more institutionalized model. For founders and management teams, this is opening new ways to fund growth, without giving up control.

But what does that look like practically, and how attractive is growth lending for companies, given its evolving state in the European market?

Growth lending is non-dilutive capital designed for sponsor-backed, growth-stage technology companies that have moved beyond product-market fit. It’s typically used by companies that are scaling revenue and operations, but don’t want to raise equity to finance every stage of growth.

As the market has evolved, lenders have expanded beyond standard term loans to offer more flexible structures, including revolving working capital facilities, customer acquisition costs (CaC) financing lines, and acquisition/M&A financing lines. These options are more closely aligned with specific growth needs and use cases, typically structured as 3-4 year amortising loans, often with an initial interest-only period.

For founders and management teams, growth lending limits dilution, enabling the business to focus on growth without always needing to raise capital.

For equity investors, growth lending can improve capital efficiency, helping companies scale without overcapitalising.

European venture capital markets have moved through some ups and downs over the last 5 years, going from rapid expansion to correction and now heading towards stabilization.

Activity peaked during 2021-22, followed by a broad correction in 2023. By 2024, conditions began to stabilize, supported by resilient investment levels and improving exit activity, including a reopening of IPO markets for several high – profile European companies, such as Klarna, Verisure and Shawbrook Bank. VC firms invested ~€60 billion per year into European technology companies during 2023-24.¹

Investment remains diversified across healthtech, energy, enterprise software, fintech, and increasingly AI and infrastructure. The UK, Germany, and France continue to account for most of the activity, while markets such as Spain, Portugal, and Greece are showing growing momentum.

By 2025, overall funding levels held stable, but deal counts declined, resulting in a greater concentration of capital in fewer, larger rounds.²

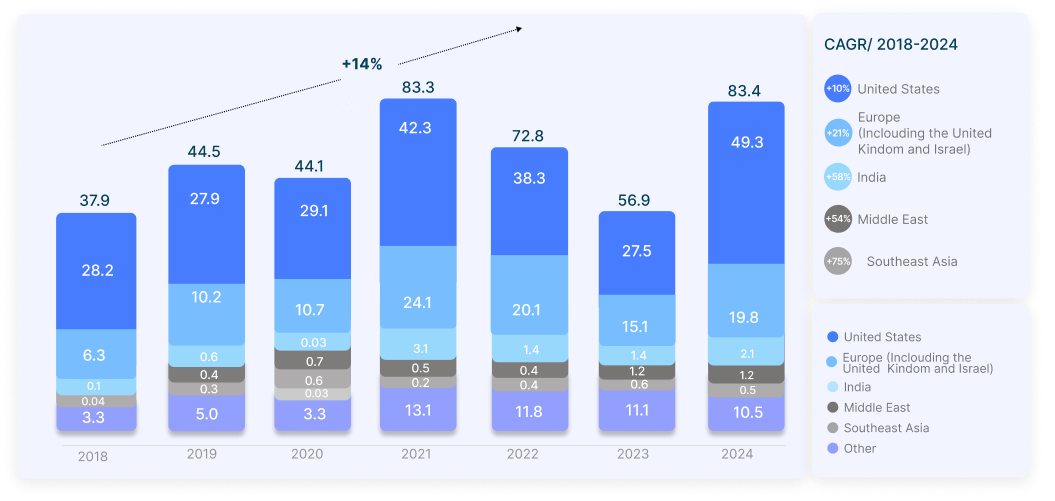

While definitions vary across sources, the direction of travel is clear: growth lending adoption in Europe is accelerating. Europe’s growth lending market was estimated at approximately US$19.8 billion in 2024, having grown at an estimated ~21% CAGR since 2018, compared with roughly ~10% CAGR in the US over the same period.³

Importantly, growth lending is being used earlier and more broadly across the company lifecycle; it’s no longer confined to late-stage companies. Throughout Europe, growth lenders are increasingly providing capital solutions tailored to different stages of company maturity, from Series B through pre – IPO. This mirrors the earlier evolution of the US market and reflects the growing institutionalization of this financing strategy.

Europe’s growth lending market today shares many characteristics with the US market a decade ago: earlier in its institutional development, still fragmented, yet increasingly relevant as companies face longer paths to liquidity.

While Europe’s overall private debt market remains roughly one-third the size of the US market, this gap accentuates the potential runway for growth across private credit, including growth lending.⁴ Whilst the deal sizes are typically smaller, as always, there are occasional outliers, notably a few large-ticket deals of €50-100M.

The primary differences between the two markets lie in how transactions are structured and executed:

The practical implication is that European growth lending often requires more bespoke structuring and jurisdictional expertise.

Europe’s private debt market remains significantly smaller than that of the US, but there are clear indications for further institutionalisation. As venture markets stabilise and late-stage valuations recover, incentives to protect dilution are strengthening, reinforcing demand for non-dilutive financing solutions.

As with any developing market, the opportunity set is best approached with an emphasis on selectivity, sponsor quality, and structuring discipline – particularly given Europe’s legal complexity and the evolving nature of the ecosystem.

At Viola Credit, we have a dedicated platform focused on providing senior secured growth capital to leading technology companies.

We view growth lending as an increasingly essential segment of private credit, playing a key role in supporting innovation across the global technology ecosystem.

If you’re considering growth debt or would like to explore how it can help accelerate your company’s growth, please connect with our team.

Deaflow: dealflow@violacredit.com

Where does growth lending fit in a financing strategy, relative to venture capital?

Growth lending helps companies reach their next milestone, whilst limiting dilution. As a proactive financing strategy, companies can finance customer acquisition, pursue strategic acquisitions, or maintain cash flow flexibility. That flexibility matters, especially in periods when equity markets are slower or more selective, scaleups can approach equity raises from a position of strength to secure better terms and well-aligned funding partners.

How does downside protection typically work in growth lending structures?

Downside protection is generally achieved through senior secured positions, conservative loan-to-value ratios, financial covenants, and active portfolio management. Underwriting will focus on a company’s path toward sustainable cash generation rather than short-term profitability.

References

Other Public Sources Used

For Companies: dealflow@violacredit.com

For Prospective Investors: investors@violacredit.com

For Marketing & Media marketing@violacredit.com

1st Floor, 18 Conduit

Street, London W1S 2XN,

United Kingdom

Landmark TLV Tower A,

Leonardo da Vinci Street, Tel Aviv

6473309 Israel

126 E 56th St,

New York, NY 10022,

United States