Private Credit Strategies: How do growth lending, venture debt and direct lending compare?

April 2026

April 2026

The private credit landscape is evolving and growing, with forecasts expecting total volumes to reach $3tn by 2028¹. As it does, so do the specialist credit strategies available, some of which are taking share from direct lending.²

One such credit strategy is venture debt; private loans specifically for high-growth, VC-backed tech companies typically in the seed to series B rounds.

Direct lending, in contrast, focuses on stable, mature companies backed by private equity. However, a strategy is emerging that benefits from the more attractive aspects of venture and direct lending: growth lending, also known as growth debt.

Growth lending has quickly become one of the most important forms of private capital supporting the innovation economy. In the US, it has been an established strategy for more than a decade, commonly used by later-stage companies as they scale toward IPO. Europe is now moving quickly in the same direction.

So, where does growth lending fit in exactly, and how do these three private credit strategies compare?

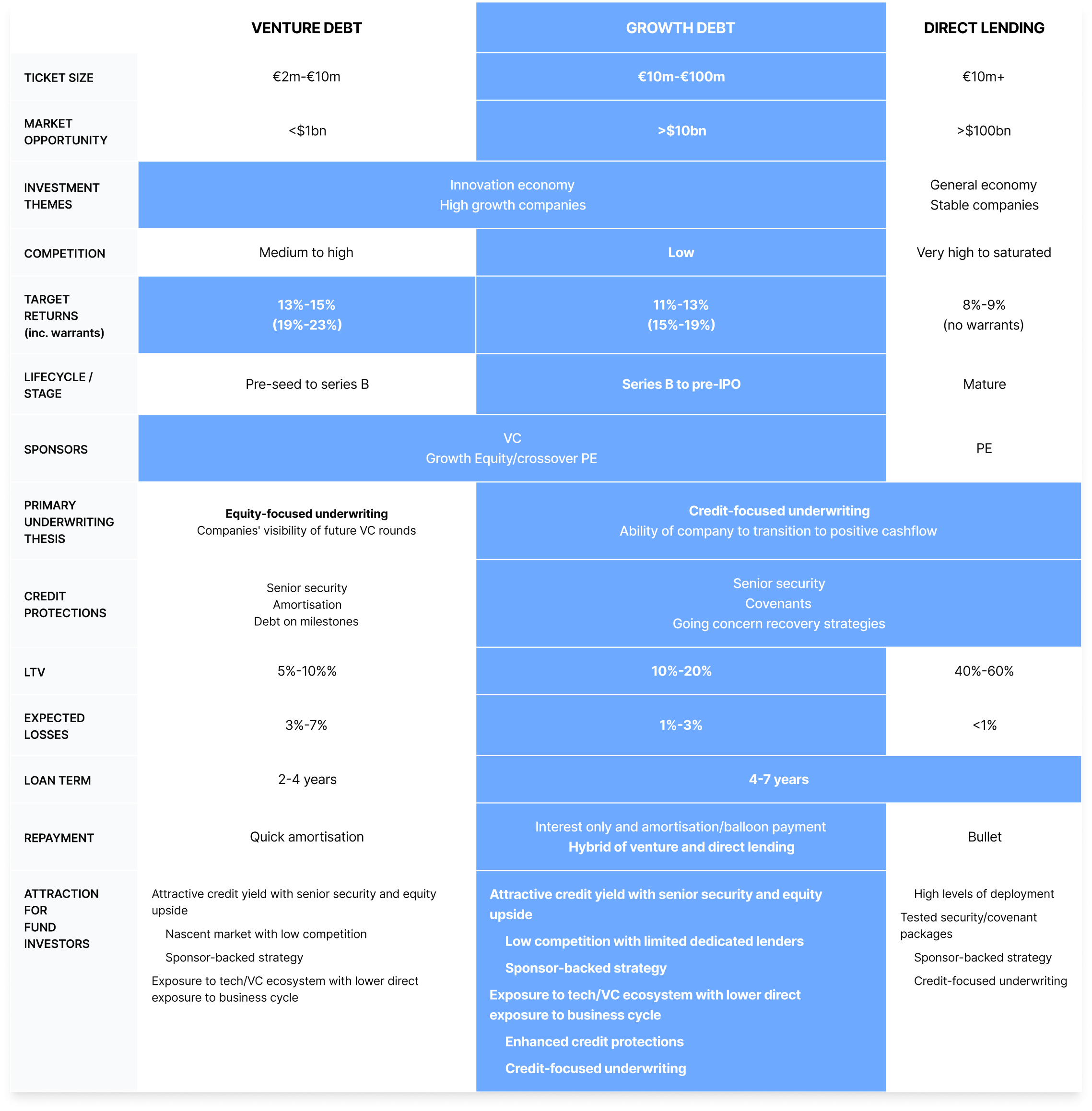

Direct lending is a form of private debt financing in which private debt funds, asset managers, or specialized lenders provide loans directly to mature, PE-backed companies without using traditional bank intermediaries.

Venture debt, or venture lending, is a non-dilutive financing option for early-stage startups that have already raised equity. It is a loan with flexible repayment terms that are tailored to a startup’s growth trajectory. Venture debt is ideal for startups looking to extend cash runway, expand, or invest in growth initiatives – without giving up additional ownership.

Growth lending or growth debt is non-dilutive, usually flexible, capital designed for sponsor-backed, growth-stage technology companies. They are typically at, or approaching, series-B to pre-IPO, where risks such as product-market fit have been mitigated. The loans are closely aligned with specific growth needs and use cases, allowing scale ups to grow without giving up further ownership.

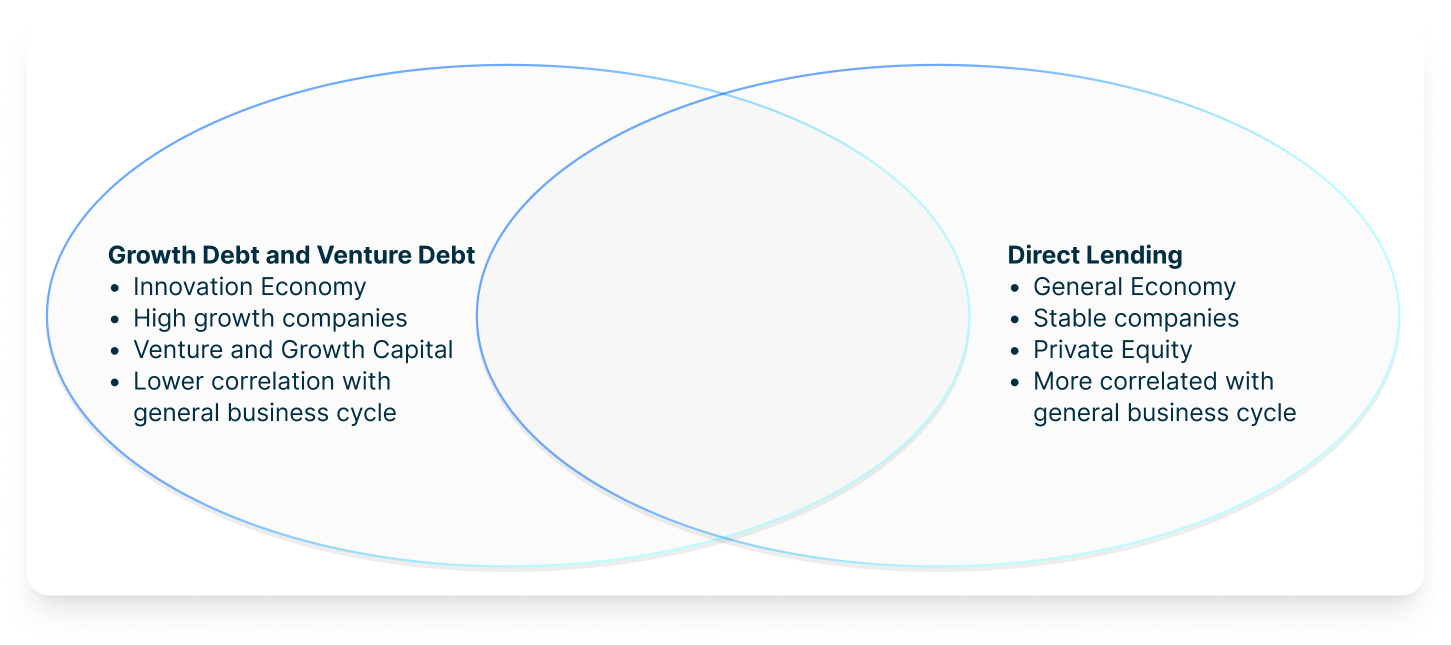

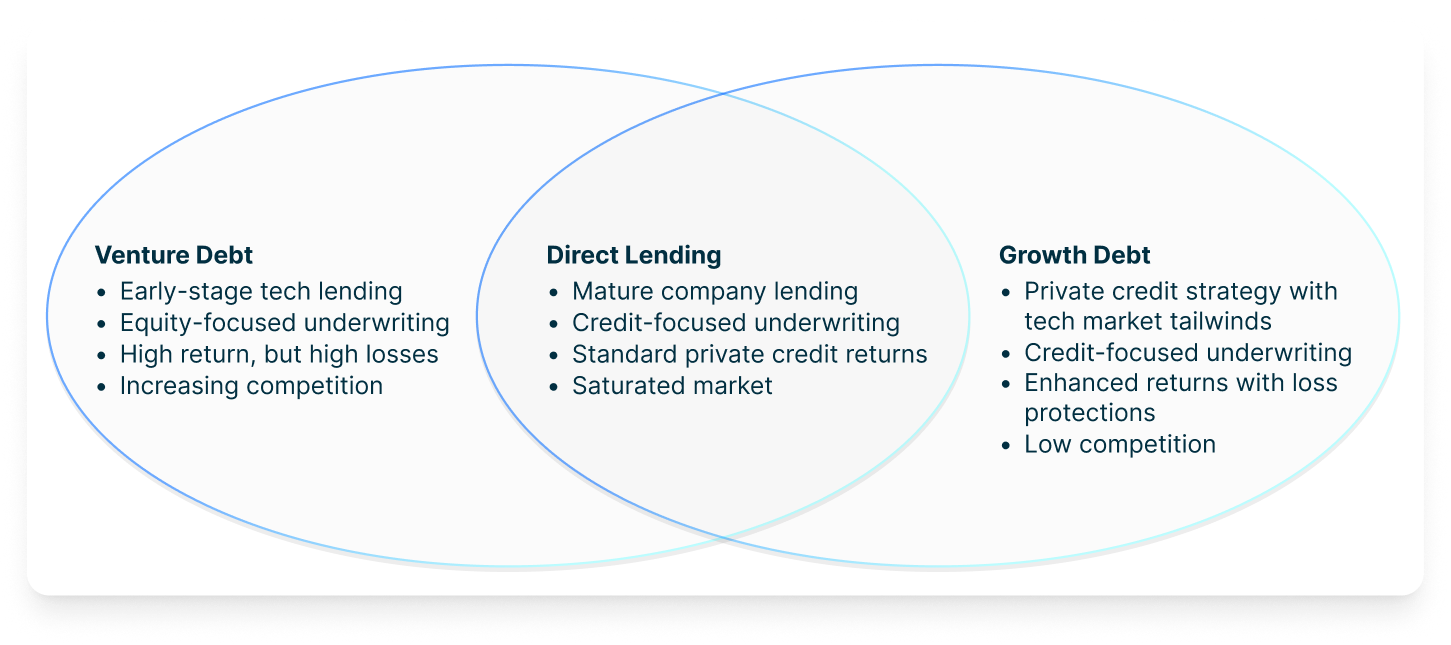

Growth, venture, and direct lending are all private credit strategies, yet they are driven by and designed for different company life stages. Direct lending is driven by LBO (leveraged buy-out) volumes executed by PE funds borrowing against more traditional, stable companies.

However, growth and venture lending benefit from exposure to the innovation economy, specifically high-growth tech companies, where the primary source of external equity is VC and growth equity.

Private Equity deal volumes have generally been closely linked to the economic cycle,³ with weak macro conditions resulting in low LBO transaction volumes and therefore low direct lending deal flow.

By contrast, studies indicate a lower direct link between general economic conditions and the VC market⁴. Accordingly, venture and growth lending volumes may prove more resilient in an economic downturn compared to direct lending.

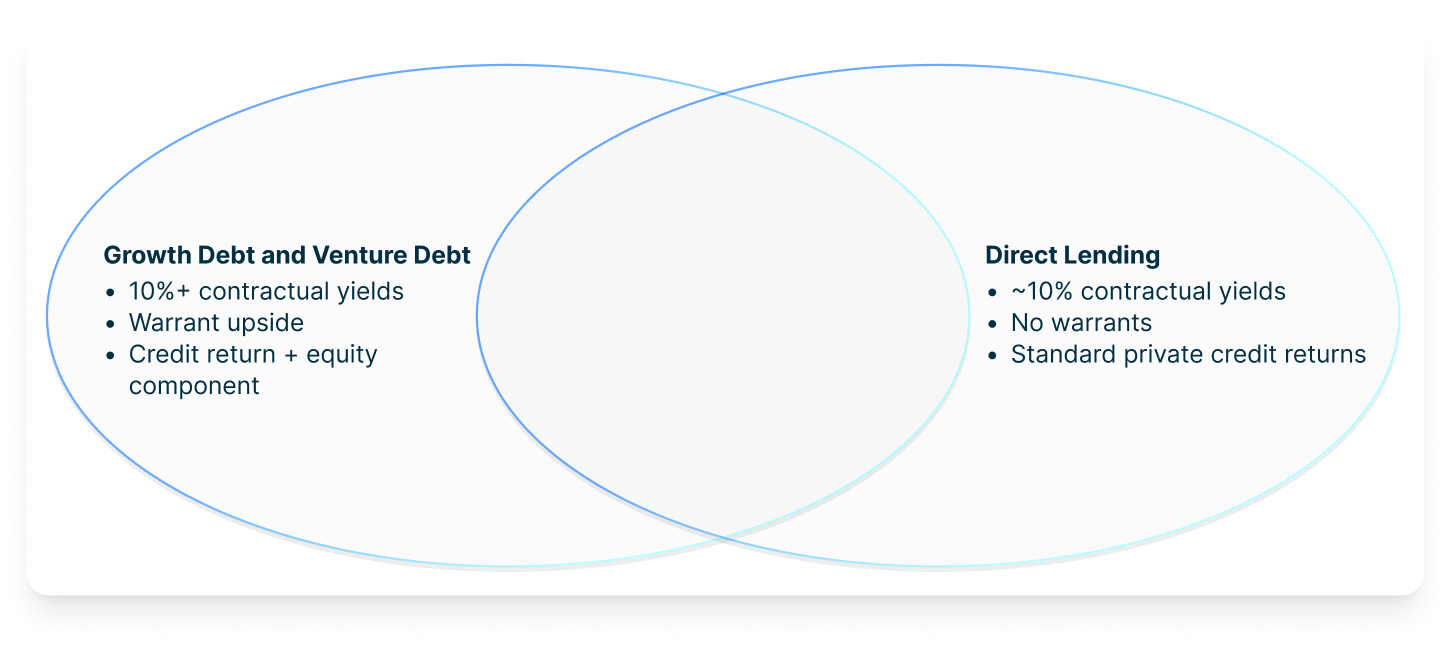

Both venture and growth lending cater to high-growth, typically cash-burning, companies that are continuing to invest in expansion. Accordingly, these strategies attract higher yields through higher coupons and greater alignment with the companies through equity upside, for example, with warrants.

Direct lending, by comparison, represents a more traditional fixed-income product with lower expected returns, but also lower risk.

Where venture lending caters to earlier-stage companies, for example, seed to series B, growth lending focuses on later-stage scale-ups, often series B to pre-IPO.

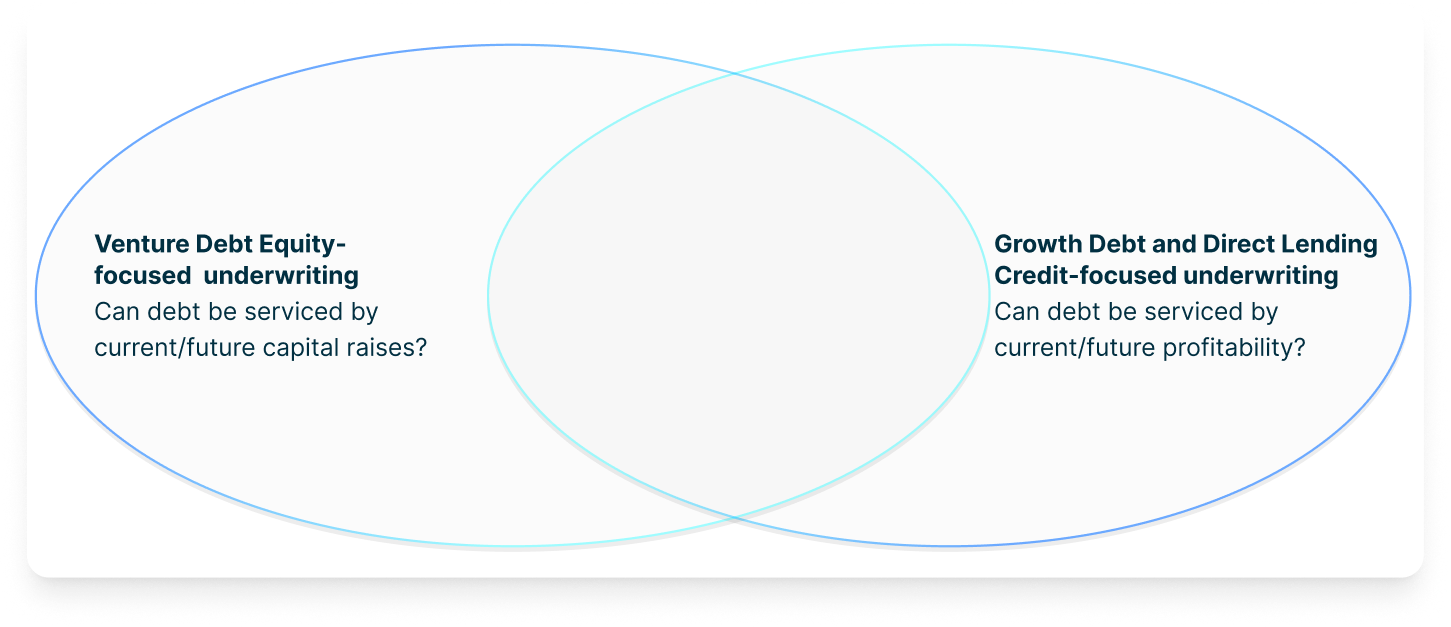

With this early-stage in mind, venture debt underwrites the ability of cash-burning companies to service and repay debt from existing liquidity (from a recent fundraise) and future liquidity (from a future fundraise) – both of which rely on equity considerations.

Compared with this, growth lending focuses on the ability of companies to transition from lower relative levels of cash burn to profitability. Then, for this profitability to service and repay debt.

In this respect, growth lending is more aligned with direct lending and its underwriting of historic and forecast profitability.

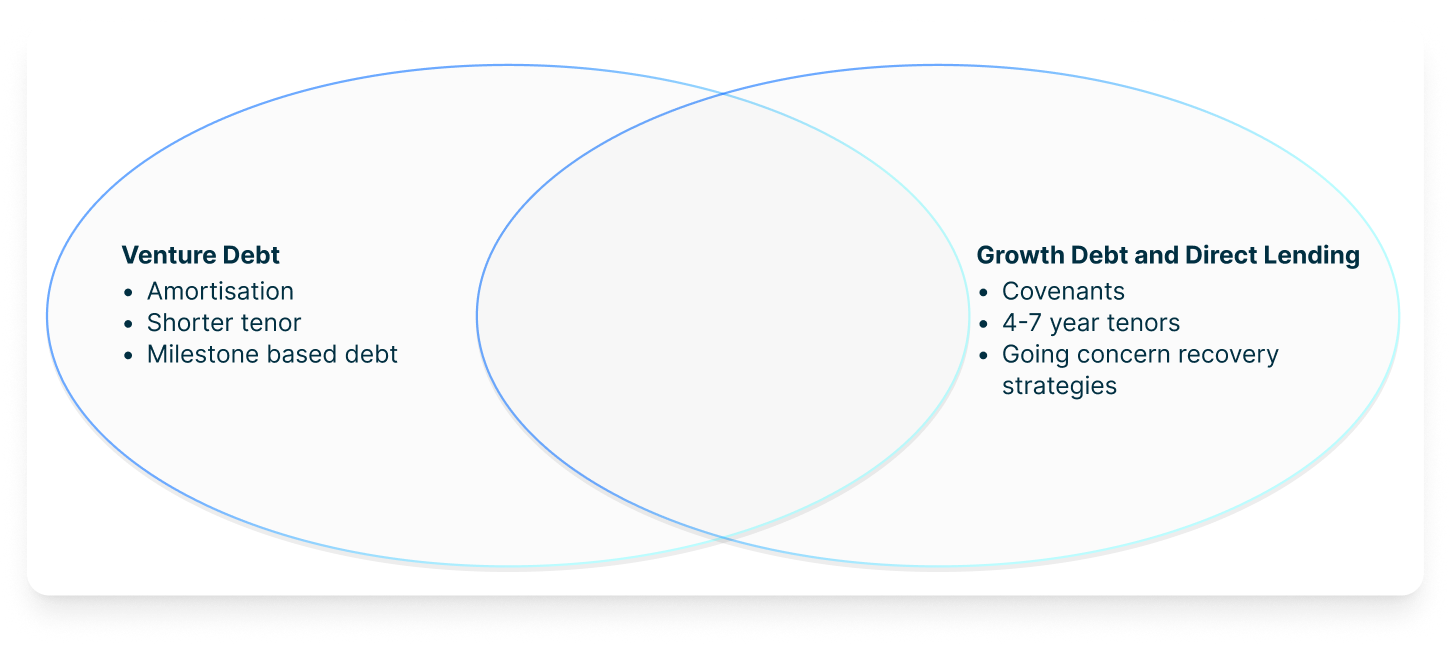

Venture debt often relies less on financial covenants and more on structural protections. Examples include shorter tenors, quick amortization, and debt granted incrementally based on performance and/or fundraising milestones.

Compared with this, growth lending, like direct lending, will structure financial covenants to ensure actual performance is within a reasonable comfort level of forecast performance.

The presence of covenants also provides the potential ability to recover through a going-concern whole business sale, as opposed to through third-party managed insolvency. This, in turn, increases potential recovery for growth and direct lending compared to venture lending.

Growth lending offers an attractive combination of enhanced returns with credit-focused underwriting and protections. This strategy allows lenders to invest in the innovation-economy, potentially offering wider portfolio diversification benefits compared to assets more directly linked to the general business cycle.

Beyond this, as an emerging specialist strategy, competition is lower with few dedicated lenders meeting European demand. As the European market develops, it is set to reward growth lending funds that have the capital, flexibility and jurisdictional expertise to navigate this ever-growing innovation space.

At Viola Credit, we have a dedicated platform focused on providing senior secured growth capital to leading technology companies.

We view growth lending as an increasingly essential segment of private credit, playing a key role in supporting innovation across the global technology ecosystem.

If you’re considering growth debt or would like to explore how it can help accelerate your company’s growth, please contact our team.

Deaflow: dealflow@violacredit.com

What makes Europe a compelling market for growth lending?

Europe’s growth lending market is earlier in its institutional development compared to the US — there are fewer participants and lower overall penetration. As companies face longer paths to liquidity, demand for non-dilutive capital is increasing, especially in scale-up companies that do not want to rely on dilutive equity rounds for funding while they tackle growth. Learn more about the evolution of the European market.

How does growth lending benefit the innovation ecosystem?

For founders and management teams, growth lending can extend runway while limiting dilution, enabling the business to focus on growth without always needing to raise capital.

For equity sponsors, growth lending can improve capital efficiency, helping companies scale without over capitalising or further ownership dilution.

And finally, for lenders, growth lending offers the potential for attractive returns with downside protection — when combined with disciplined structuring and underwriting.

1 ‘Private credit – primed for growth as LBOs revive, ABF opportunities accelerate’ – Moodys.com

2 ‘Private Credit Outlook 2025’ – withintelligence.com

3 ‘Rising to the Challenge: Slowing Investment Cycles Test Private Equity Strategies’ – spglobal.com

4 ‘Venture Capital Booms and Startup Financing’ – Harvard Business School working paper: William Janeway (Cambridge University), Ramana Nanda (HBS), Matthew Rhodes-Kropf (MIT)

For Companies: dealflow@violacredit.com

For Prospective Investors: investors@violacredit.com

For Marketing & Media marketing@violacredit.com

1st Floor, 18 Conduit

Street, London W1S 2XN,

United Kingdom

Landmark TLV Tower A,

Leonardo da Vinci Street, Tel Aviv

6473309 Israel

126 E 56th St,

New York, NY 10022,

United States